“You’re not selling software. You’re selling transformation.”

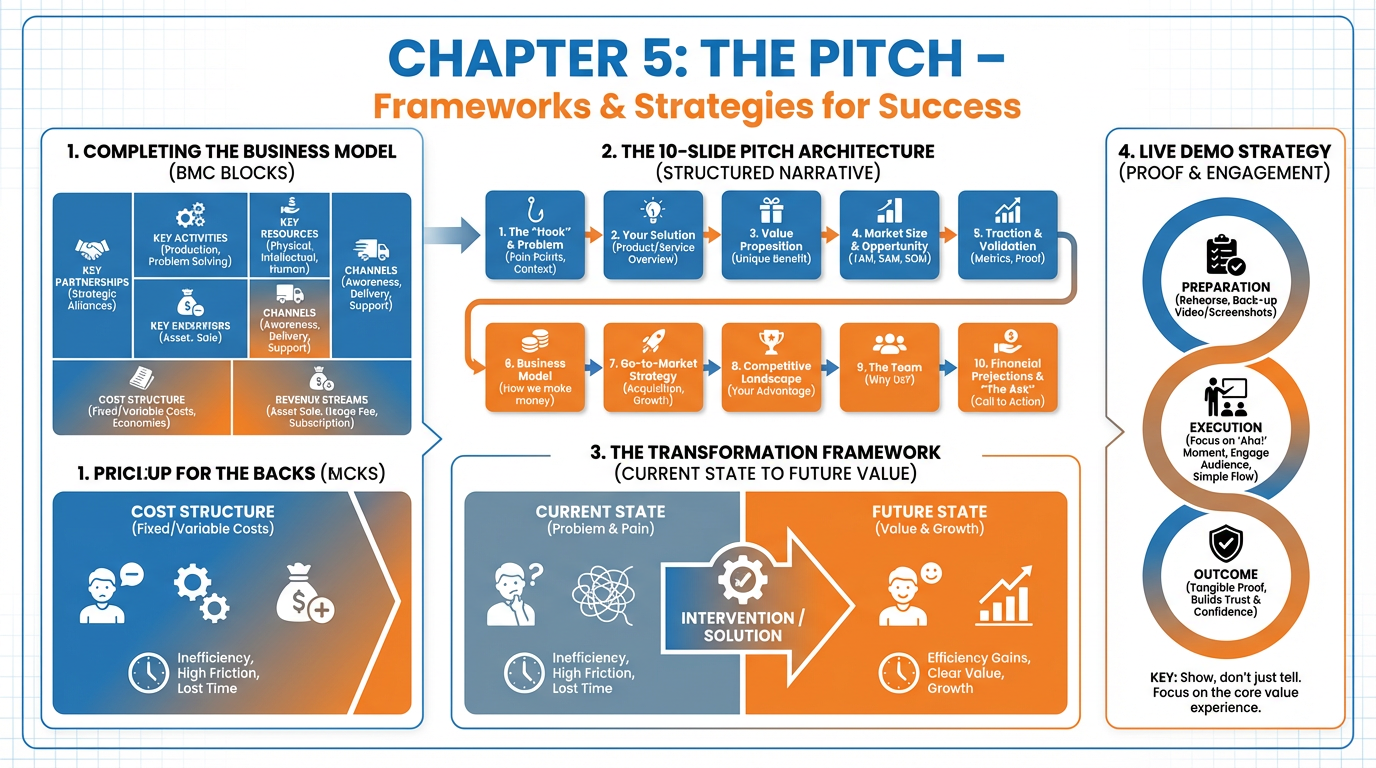

Figure 1:Chapter 5 in one frame: the five remaining Business Model Canvas blocks, the six-step Transformation Framework, the 10-slide pitch architecture, and the live demo principles that separate funded founders from the rest.

1Learning Objectives¶

By the end of this chapter, you will be able to:

Complete all nine blocks of the Business Model Canvas with investor-grade specificity, including Channels, Customer Relationships, Revenue Streams, Key Resources, Key Activities, and Key Partnerships.

Articulate the distinction between “entrepreneur thinking” and “developer thinking” and explain why investors fund businesses, not apps.

Apply the six-step Transformation Framework to convert a product description into a compelling investor narrative.

Build a 10-slide pitch deck whose architecture follows the logic of investor cognition.

Plan and execute a live demo that proves your product exists and that you can ship.

Respond to the five categories of investor objection with honest, practiced, and distinction-aware answers.

25.1 Finishing the Business Model Canvas¶

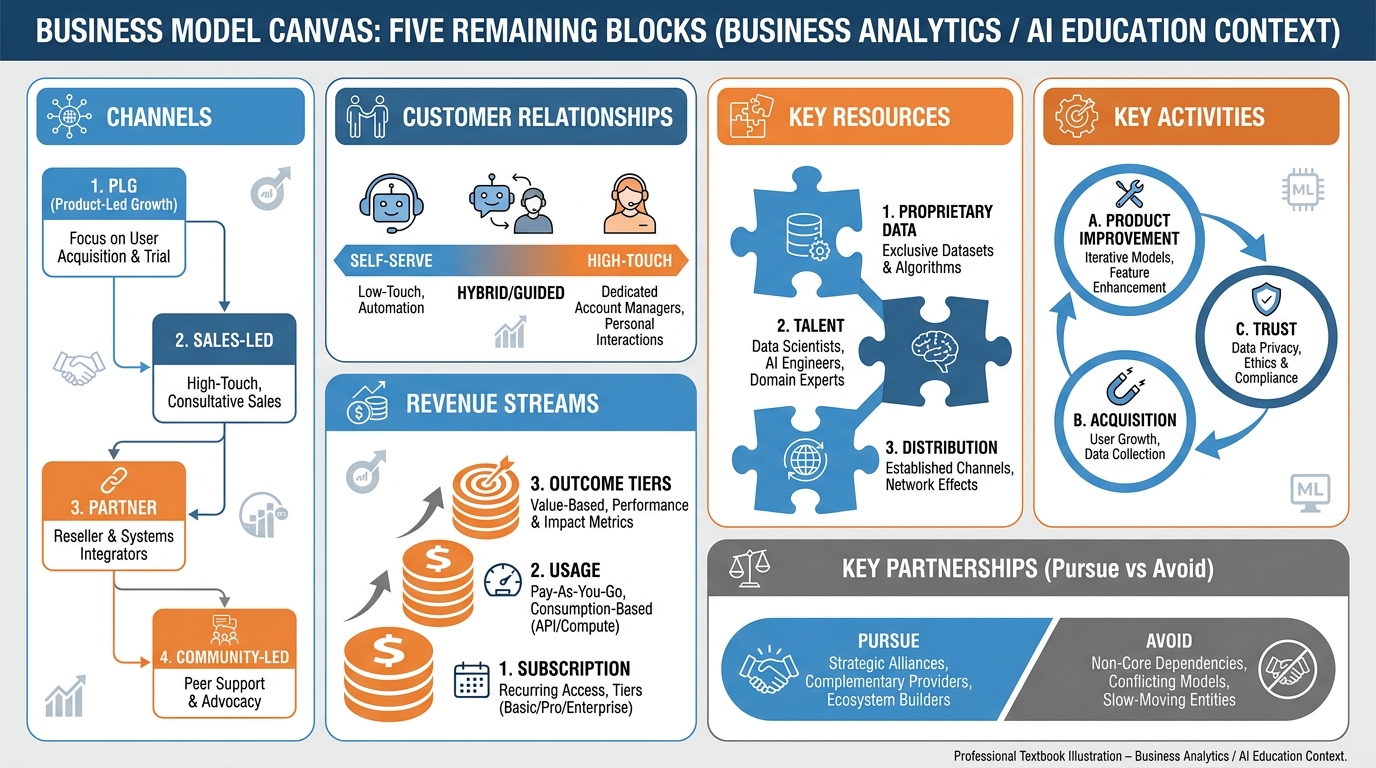

Figure 2:The right side of the Business Model Canvas is where strategy meets execution. Most student teams can describe their value proposition (Chapter 2) and their customer segments (Chapter 3). Fewer can defend Channels, Revenue Streams, and Key Resources with investor-grade specificity. This section closes that gap.

In Chapters 2 through 4, you built the foundation: a pain-first value proposition, a precisely defined Ideal Customer Profile, and a unit economics model that separates viable businesses from expensive hobbies. The Business Model Canvas has nine blocks. You have rigorously addressed four. This section completes the canvas — not as a form-filling exercise, but as a strategic pressure test.

2.1Channels: How Customers Find You and How You Reach Them¶

A channel is the route through which your value proposition reaches the customer. The choice of channel is not a marketing decision — it is a structural one that determines your CAC, your sales cycle, and whether your go-to-market motion matches your ICP.

The five primary channel motions for AI-native businesses are:

Direct (Field Sales): You hire salespeople who call, email, and close deals. High-touch, high-CAC. Works when ACV (Annual Contract Value) exceeds roughly $25,000, because the economics of a human sales cycle require a large enough deal to justify the cost. Enterprise AI compliance tools, custom model deployments, and agentic workflow platforms often go direct.

Partner / Channel Reseller: You sell through a third party — a systems integrator, a consulting firm, or a platform marketplace (e.g., Salesforce AppExchange, AWS Marketplace). Lower upfront CAC but margin compression and dependency risk. Appropriate when your ICP already buys through that partner and when your product extends rather than competes with the partner’s offering.

Product-Led Growth (PLG): The product sells itself. Freemium tiers, viral loops, and bottom-up adoption let individual users discover and champion your product inside their organization. PLG works when the value is immediately demonstrable, when switching costs are low enough to get someone to try but high enough to keep them, and when the per-seat expansion model is in place. Cursor, Notion, and Figma all scaled primarily through PLG before adding enterprise sales.

Sales-Led Growth (SLG): A traditional top-down motion in which a centralized buying decision is made by economic buyers (VP, CTO, CFO). Works for regulated industries, multi-department deployments, and any context where legal review or security certification is required before a user can even touch the product.

Community-Led Growth: The community — a Slack group, Discord server, an open-source repository, a newsletter, or a cohort program — drives product adoption. Developer tools, AI infrastructure products, and platforms targeting founders or operators often use community-led motions because trust is established through peer endorsement before commercial engagement.

Matching Channel to ICP: The critical principle is fit. A PLG motion for a product whose ICP is a risk-averse CFO at a regulated bank will fail. A field-sales motion for a $29/month tool targeting freelancers will bleed CAC. The channel must match where your ICP already goes to discover solutions, how much trust is required before they buy, and what price point can support the friction of that channel.

2.2Customer Relationships: Self-Serve vs. High-Touch¶

Customer relationships define the type of interaction you maintain with each customer segment. The spectrum runs from fully automated self-serve (no human involvement) to dedicated personal assistance (a named human owns the relationship).

Where AI changes the cost curve is significant. Self-serve used to mean “the customer is on their own.” AI-powered onboarding, in-product assistants, automated QBRs (Quarterly Business Reviews), and AI-generated success playbooks now allow a company to deliver what previously required a customer success team — at near-zero marginal cost per customer.

The relationship model also affects NPS, churn, and expansion revenue. Customers who are left to figure things out alone churn when the first obstacle appears. Those who are over-managed with weekly check-in calls resent the intrusion and churn when they realize they never needed you that much. The goal is calibrated relationship intensity: automated for the long tail, tiered personal attention for accounts where lifetime value justifies the spend.

2.3Revenue Streams: Subscription, Usage, and Outcome¶

Three dominant revenue architectures exist for AI-native businesses:

Subscription (Seat-Based or Flat): Predictable recurring revenue. Easy to model. Customers know what they’ll pay. Risk: the “shelfware” problem — customers pay but don’t use, then churn at renewal because they cannot justify the cost.

Usage-Based (Consumption): Customers pay for what they use — API calls, tokens processed, hours of automation, documents analyzed. Aligns incentives (you win when they win), scales naturally with customer success, but introduces revenue volatility that makes financial forecasting harder and sometimes spooks investors unfamiliar with the model.

Outcome-Based: The most ambitious and hardest to structure. You charge a percentage of the value created — cost savings delivered, revenue generated, time reclaimed. Works when outcomes are measurable and attributable, when your contract terms allow for audit rights, and when trust in your methodology is established. Rarely viable for early-stage companies without strong references.

Tier Design Principles: When designing pricing tiers, three rules apply. First, tiers should expand with value delivered — the customer who uses your product more pays more because they’re getting more. Second, the free or starter tier should create genuine habit, not just exist as a demo environment. Third, the jump from one tier to the next should be triggered by a natural usage ceiling that the customer feels organically, not by an arbitrary limit that feels like a trap.

2.4Key Resources: What Competitors Cannot Cheaply Replicate¶

Key Resources are the assets your business model requires to deliver the value proposition. For AI-native businesses, the critical resource question is not “what do we have?” but “what do our competitors not have and cannot easily acquire?”

The most defensible resources in AI businesses:

Proprietary data: Training sets, behavioral data, longitudinal clinical records, user-generated outputs that improve the model. This is the deepest moat available.

Talent: Not general engineers — domain-specific researchers, practitioners who understand the problem at a clinical or legal or engineering depth that allows the AI to be trusted, not just used.

Distribution relationships: Customer relationships, integration partnerships, and embedded workflows that would require months or years to rebuild.

Regulatory position: Certifications, licenses, and approvals (HIPAA, SOC 2, FDA clearance, FedRAMP) that create a compliance barrier for competitors entering your market.

2.5Key Activities: The Three Things You Must Be Great At¶

Key Activities are what you must execute excellently for the business model to function. The mistake most founders make is listing too many — twelve activities that are equally important means none of them are actually priorities.

For an AI-native business, the three that matter most are typically:

Model or product improvement: Continuously making the core AI capability better based on customer feedback, new data, and infrastructure investment.

Customer acquisition and activation: Getting the right customers in the door and making sure they experience value before their attention shifts elsewhere.

Trust and compliance: In regulated markets, maintaining certifications and proactively managing data privacy obligations. In unregulated markets, building the reputation and reference base that reduces buyer risk.

2.6Key Partnerships: Who You Need — and Who to Avoid Depending On¶

A partnership is a supplier, platform, or co-marketing relationship that is structurally necessary for your business to function. The risk of a key partnership is dependency: if the partner changes terms, goes out of business, or becomes a direct competitor, your business is exposed.

Partnerships to pursue: integration partners whose platform your ICP already lives inside, distribution partners who have trust with your buyer already established, and infrastructure providers with strong contractual stability.

Partnerships to avoid depending on: any single large platform whose API terms can change without notice, any partner whose roadmap could make your product redundant, and any channel partner whose incentives are not aligned with your customers’ success.

35.2 Investors Fund Businesses, Not Apps¶

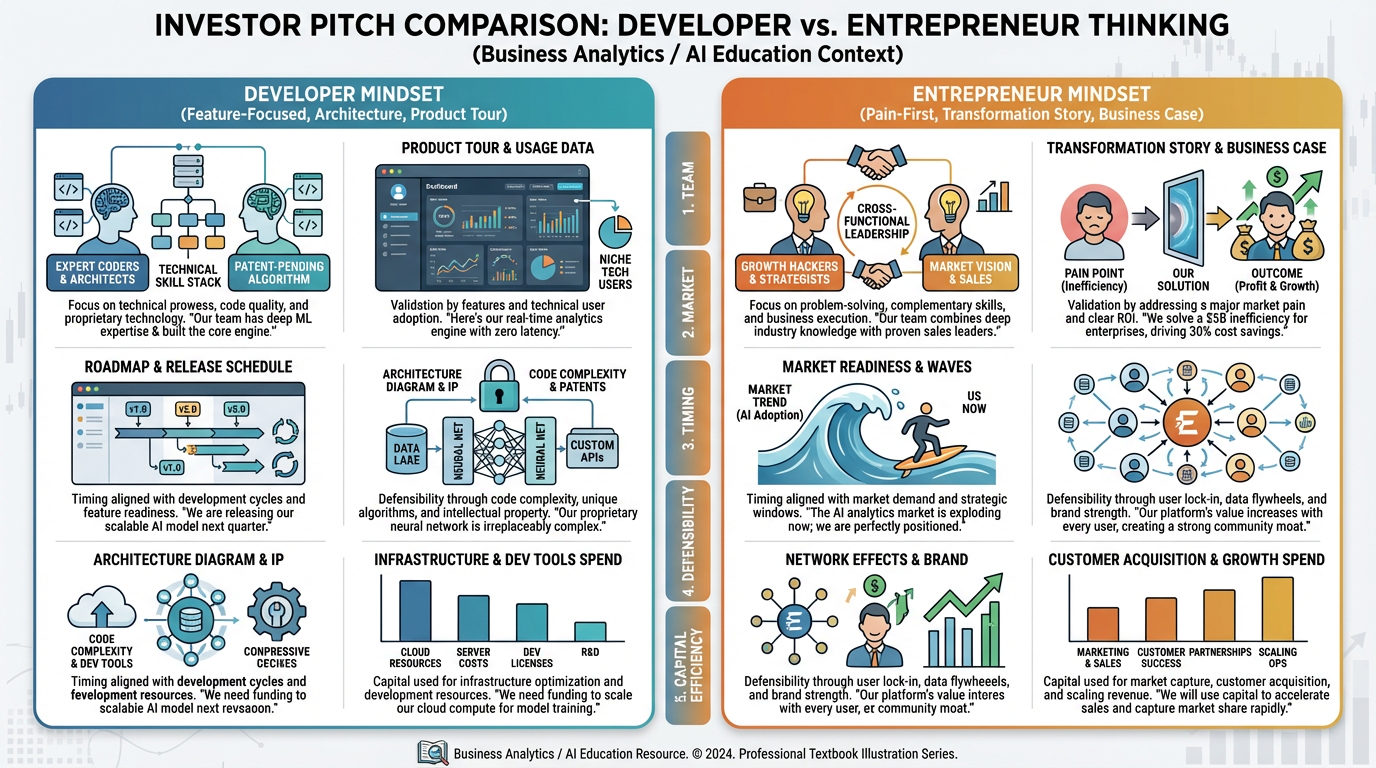

Figure 3:The gap between what developers present and what investors evaluate. Founders who close this gap raise faster and on better terms.

There is a failure mode that appears so frequently in student and early-stage pitches that it deserves its own frame: developer thinking versus entrepreneur thinking.

Developer thinking frames problems as technical challenges and solutions as features. A developer-thinker’s pitch describes what the product does, walks through the interface, explains the architecture, and concludes with a pricing page. The implicit assumption is: “If you understand what it does, you will want to buy it.”

Entrepreneur thinking frames problems as market opportunities and solutions as value delivered to specific humans who will pay for that value. An entrepreneur-thinker’s pitch opens with the pain, proves the pain is real and widespread, introduces the solution as a mechanism for transformation, and closes with evidence that the company can win.

Investors are not evaluating your code. They are evaluating whether a business exists around your code. The five dimensions every investor assesses — often before slide 6 — are:

Team: Can these founders learn fast enough to find the real opportunity even if their initial hypothesis is wrong? Domain expertise, past evidence of execution, and cofounder dynamics all factor in.

Market: Is the total addressable market large enough to justify venture scale, or is this a lifestyle business dressed as a startup? Investors want to see 10M ARR.

Timing: Why now? What has changed in the last two years — technically, regulatorily, or behaviorally — that makes this the right moment for this solution?

Defensibility: If this works, what prevents the incumbent from copying it? What prevents a well-funded entrant from outspending you?

Capital Efficiency: How much capital is required to reach a meaningful proof-of-concept, and what will the burn rate look like post-raise? The lower the capital required to prove the thesis, the more attractive the risk-adjusted bet.

The five questions every pitch must answer before slide 6:

Who is in pain and how do you know?

How big is the universe of people with that pain?

Why hasn’t this been solved before — or why is your solution 10x better than what exists?

What does success look like in 18 months, and what milestone does this raise fund?

Why are you the team to do this?

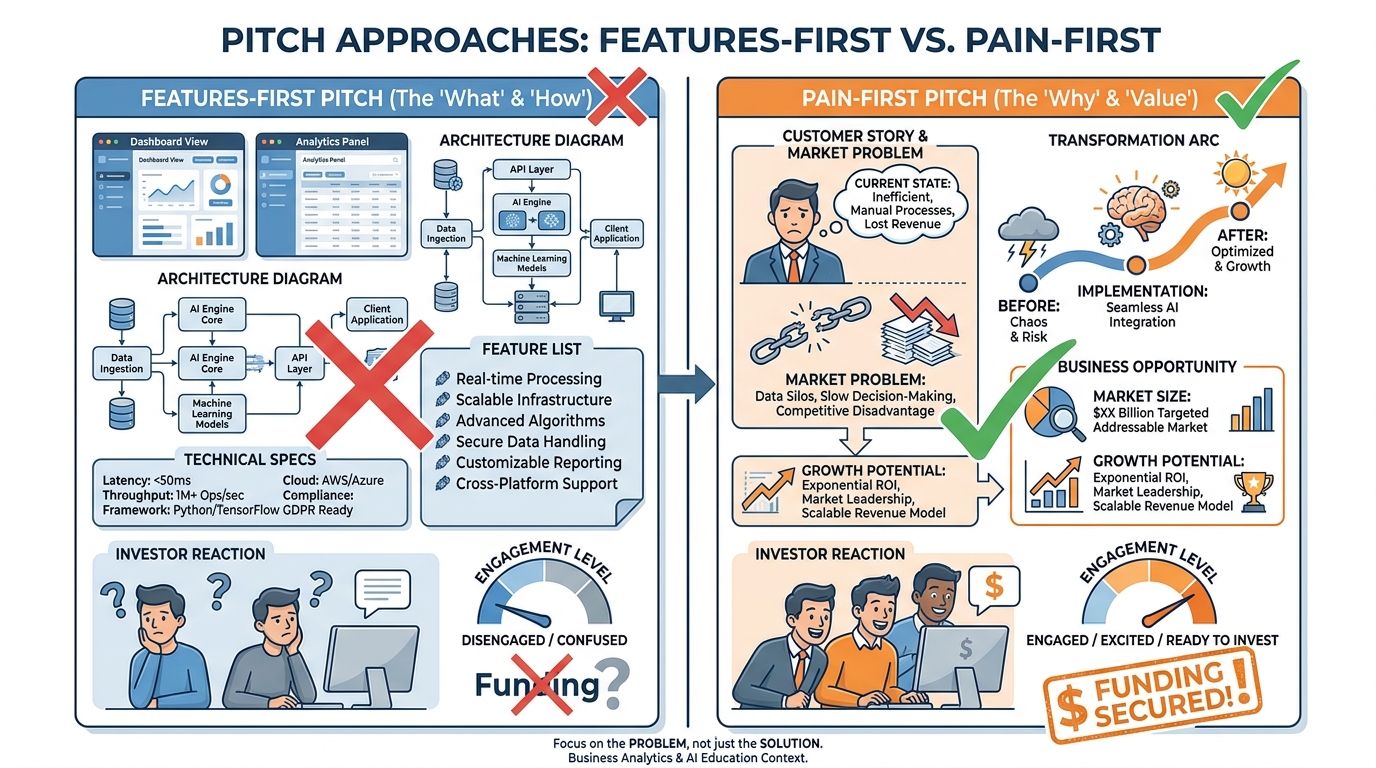

Figure 4:Features-first versus pain-first pitch structure. The investor’s brain processes pain stories as business opportunity and feature lists as product roadmaps. One signals a business. The other signals a demo.

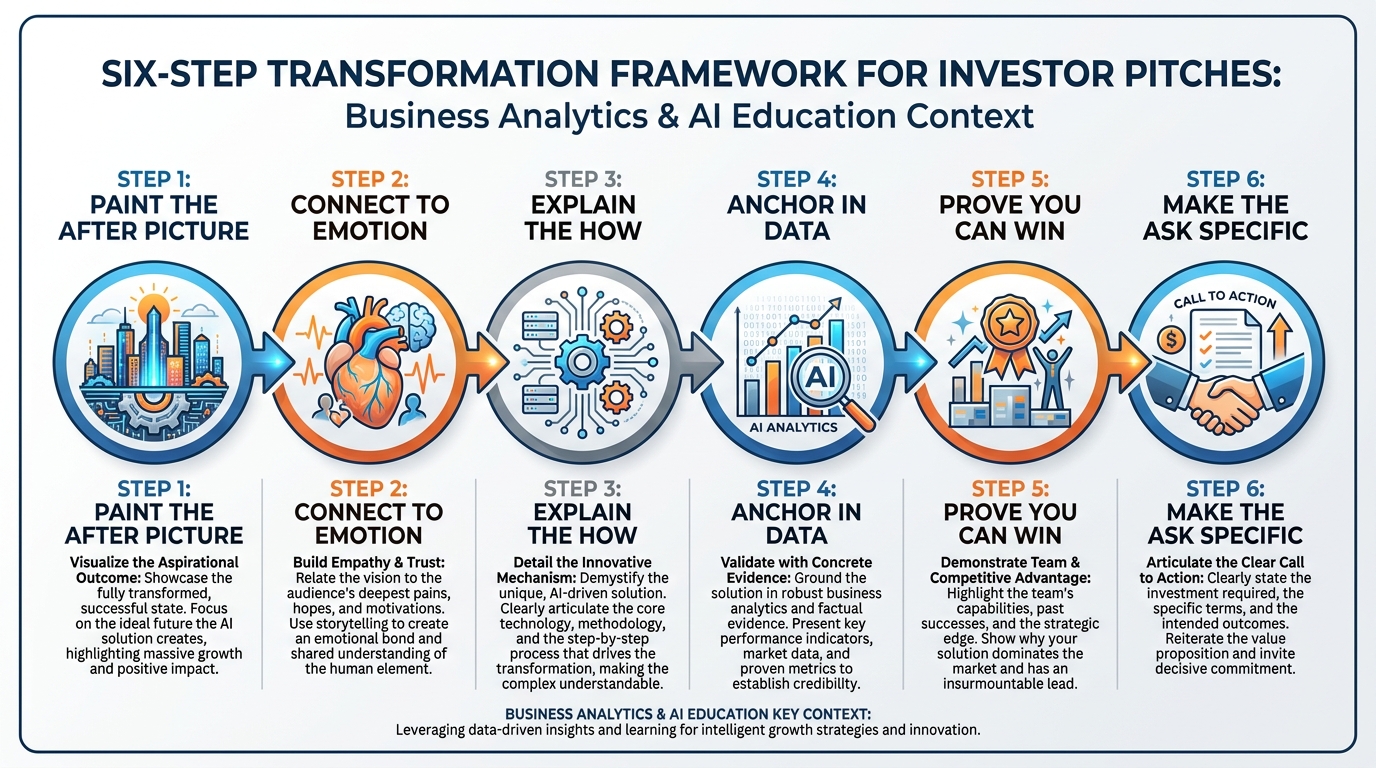

45.3 The Transformation Framework¶

Figure 5:The six-step Transformation Framework converts a product description into a story that investors want to fund. Each step has a distinct job. Missing any one of them weakens the whole.

A pitch is not a product tour. It is a story about transformation — the world before your company, and the world after. The Transformation Framework provides a repeatable structure for building that story.

Step 1 — Paint the After Picture

Start with the world your customer inhabits after your product solves their problem. Not what your product does — what life is like when it works. A freight logistics company whose CFO no longer loses sleep over invoice reconciliation. A healthcare administrator who discharges patients 40 minutes faster because prior authorization is automated. Before the investor cares about how you build it, they need to viscerally desire the outcome.

Step 2 — Connect to Emotion

The after picture must connect to something the investor has felt or can imagine feeling. Frustration, anxiety, embarrassment, missed opportunity — these are the emotional raw materials of a compelling pitch. Data creates credibility; emotion creates investment. The best pitches pair a specific human story (a named person, a real situation) with the broader market thesis.

Step 3 — Explain the How

Now — and only now — introduce the mechanism. How does your product create the transformation you described? This is where the technology lives in the story. Keep it at the level of “what it does” rather than “how it’s built.” The mechanism should feel inevitable: of course this is how you solve that problem.

Step 4 — Anchor in Data

The story needs evidence. Market size data, customer quotes, retention numbers, a compelling case study, or early NPS scores — whatever you have that proves the problem is real, the solution works, and people are willing to pay. Data without story is a spreadsheet. Story without data is a pitch from someone who hasn’t done the work. You need both.

Step 5 — Prove You Can Win

This is the most underserved step in student pitches. Proving you can win requires answering the “why you?” question with specificity: proprietary access to data, domain expertise that took years to build, a distribution relationship competitors cannot replicate, or early traction that proves market validation. Generic claims (“we have a great team”) do not satisfy this step.

Step 6 — Make the Ask Specific

“We are raising a round” is not an ask. “We are raising 10M cap, which funds us to $750K ARR by Month 18, at which point we will have enough proof to raise a Series A at better terms” is an ask. Investors respect founders who have done the capital planning. The specific ask signals financial sophistication, not desperation.

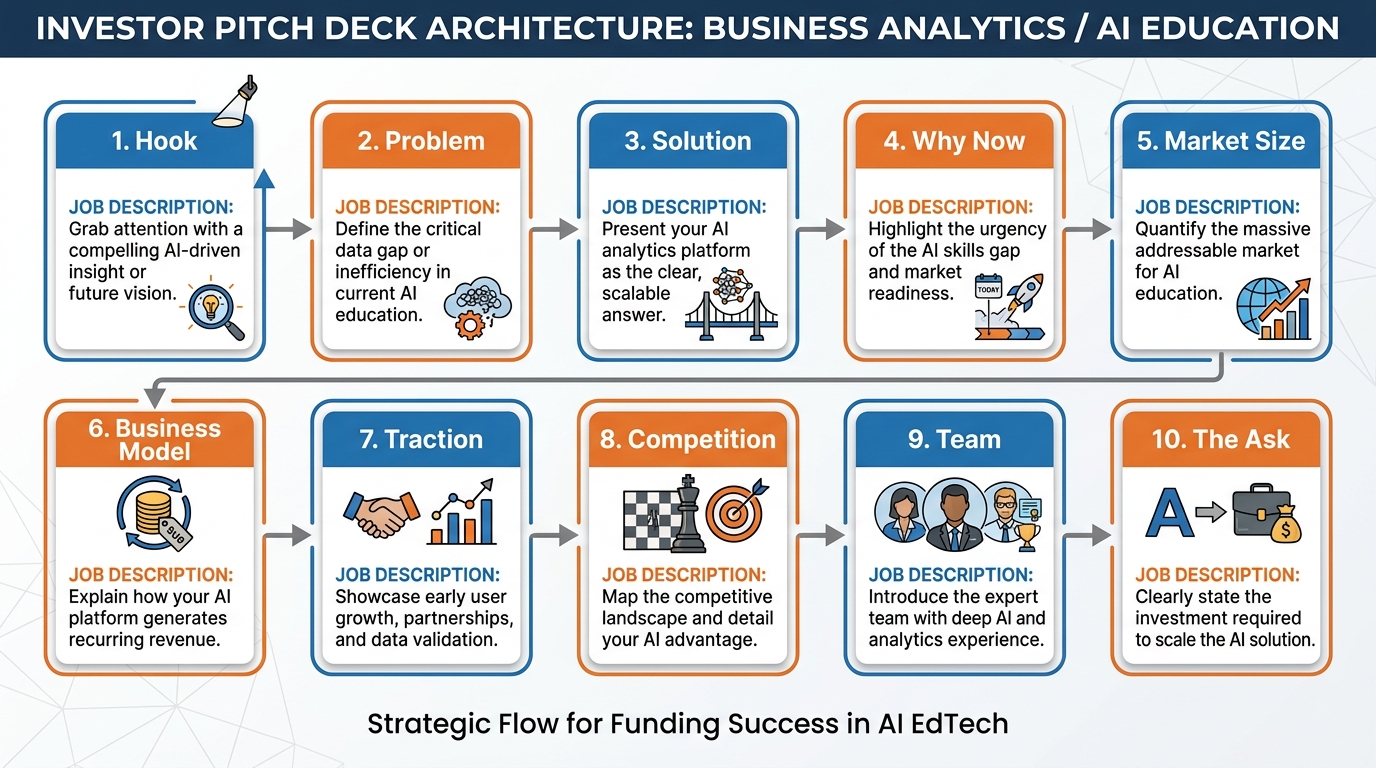

55.4 The 10-Slide Architecture¶

Figure 6:The 10-slide architecture maps the investor’s cognitive journey from “Who are you?” to “Where do I sign?” Each slide has one job. Slides that try to do two jobs dilute both.

Every investor has seen hundreds of pitch decks. They have also sat through hundreds of pitch meetings. Pattern recognition is working for and against you: for you, because a well-structured deck signals professional maturity; against you, because any structural deviation creates cognitive friction that breaks trust.

The 10-slide architecture below is not a template — it is a sequence of investor questions answered in the order investors ask them.

| Slide # | Slide Name | Job It Must Do |

|---|---|---|

| 1 | The Hook | Make the investor lean forward. Open with the most compelling version of the problem — a striking statistic, a human story, or a moment that reframes how they see the market. Do not introduce the company name until the investor is already engaged. |

| 2 | The Problem | Define the pain with specificity. Quantify it. Identify who feels it and how often. Make the investor feel the friction your customer lives with every day. |

| 3 | The Solution | Introduce your product as the answer to slide 2. One sentence of what it does. Then show, not tell — a screenshot, a diagram, or a live product moment. |

| 4 | Why Now | Explain the enabling change. What has shifted technically, regulatorily, or behaviorally in the recent past that makes this the right moment? This slide prevents the “why hasn’t someone done this?” objection from forming. |

| 5 | Market Size | TAM → SAM → SOM. Use bottoms-up math, not top-down market research citations. Show how you calculated the numbers, not just what they are. |

| 6 | Business Model | How you make money. Pricing, channel, revenue architecture. Keep it to the essential structure — not a full pricing page, but enough to show you have thought through unit economics. |

| 7 | Traction | Your strongest evidence that this is real. Revenue, LOIs, pilot results, retention data, user counts. Traction is proof of demand. If you have none, use customer discovery evidence — recorded interviews, survey results, signed waitlists. |

| 8 | Competition | A 2×2 or positioning map that shows where you sit relative to alternatives. Never say “we have no competitors” — this tells investors you haven’t done the research or that the market doesn’t exist. |

| 9 | Team | Why you. Relevant experience, domain expertise, and evidence of prior execution. Include any advisors whose credibility transfers. Keep it to the two or three facts per person that directly connect to the problem you’re solving. |

| 10 | The Ask | Amount, instrument (SAFE, convertible note, equity), cap or valuation, use of funds, and the milestone this capital reaches. One slide. Maximum clarity. |

65.5 Show, Don’t Tell: The Live Demo¶

Figure 7:Demo choreography: the sequence of a live demo is as important as the technology itself. Investors are watching for three things — does it work, does the founder understand what they’re building, and does the product feel inevitable?

A working demo is worth ten slides of mockups. Mockups are promises. A live product is evidence. The moment an investor sees a real product doing a real thing, the cognitive burden of “does this actually work?” disappears — and their attention shifts to “can this team scale it?”

6.1What to Show¶

Show the full journey from input to output — the moment that makes the investor think “I can’t believe this is possible.” For an AI product, that moment is usually the first time the model does something that feels like magic: summarizing a complex document in three seconds, generating a contract clause on demand, flagging a fraudulent transaction in real time. Build the demo to reach that moment as quickly as possible.

6.2What to Skip¶

Skip the login screen. Skip the account settings. Skip anything that doesn’t directly demonstrate value. Every second of a demo that doesn’t deliver a “wow” moment is a second where the investor’s attention is available to drift.

6.3What to Never Debug Live¶

Never fix a broken demo during a pitch. If something fails, acknowledge it calmly (“let me show you the same thing in our test environment”), move to a backup, and keep the energy steady. The worst demo failures are not technical — they are emotional: the founder who panics, who becomes visibly frustrated, who loses the narrative thread while trying to troubleshoot. Composure under pressure is itself a signal investors are watching for.

6.4Using Claude Code to Prototype in Hours¶

Modern AI coding environments — including Claude’s coding interface — can produce functional proof-of-concept demos in hours rather than weeks. A working prototype does not need to be production-grade. It needs to demonstrate the core mechanic: that your AI can do the thing you claim it can do. Build the demo first. Build the infrastructure later.

6.5The Narrator Mode Rule¶

Never go silent during a demo. The investor does not know what they’re looking at unless you tell them. Use “narrator mode”: describe what is happening and why it matters as it happens. “I’m entering a sample contract here — this would normally take a paralegal 45 minutes to review. Watch what happens in the next 8 seconds.” Narration converts a product demonstration into a story, and stories are retained.

Deep Dive: Building a Demo-Ready Prototype in One Weekend

Hour 1–2: Define the one core mechanic you want to demonstrate. Write it as a user story: “As a [user], I want to [action] so that [outcome].” Resist the temptation to add features.

Hour 3–6: Use an AI coding environment to scaffold the application. Prompt for the core function first, then the UI wrapper. Focus entirely on the “magic moment” — the output that will make the investor lean forward.

Hour 7–10: Test the demo path end-to-end at least 20 times. Remove every step that is not the magic moment. Add a fallback state (a recorded version of the output) for any step that might fail.

Hour 11–14: Practice the narration. Record yourself demoing. Watch it back. Cut anything that doesn’t add to the story.

Hour 15–16: Prepare three backup states: a live demo, a local version without internet dependency, and a screen recording. Know exactly when to switch.

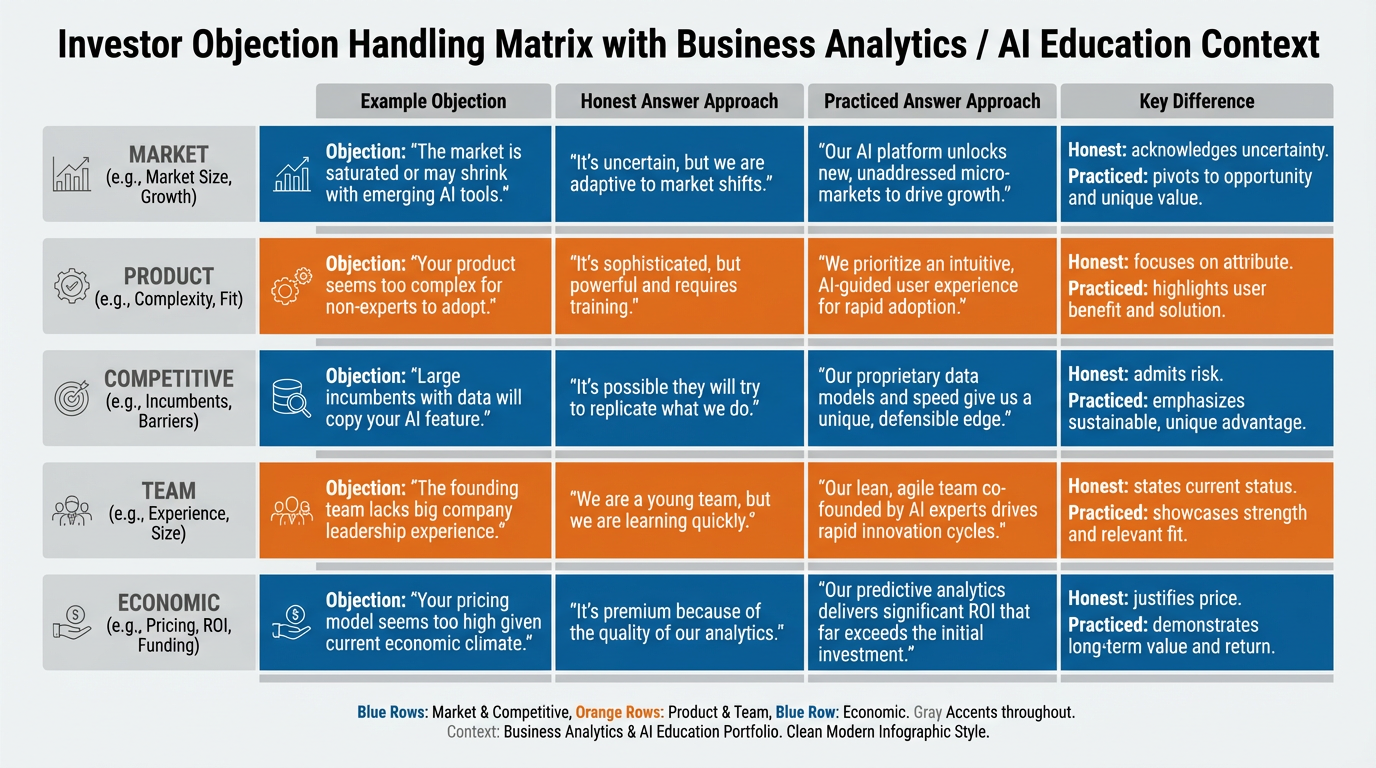

75.6 Handling Objections¶

Figure 8:The objection matrix. Every objection has a surface form and an underlying concern. Answering the surface form without addressing the underlying concern is the most common Q&A failure mode.

Objections are not rejections. They are questions that an investor is not comfortable asking directly. The founder who hears an objection as an attack — and responds defensively — loses the room. The founder who hears an objection as an opportunity to demonstrate sophistication and honesty wins it.

Investor objections cluster into five categories:

Market Objections

“The market isn’t big enough” / “I don’t think enterprises will pay for this”

Honest answer: “Our current bottoms-up TAM calculation shows Y relies on these three assumptions, and we can defend each of them.”

Practiced answer: Agree with the constraint, then reframe: “You’re right that the initial segment is narrow. That’s deliberate — we’re going after the highest-pain, fastest-paying buyers first. The adjacent segment is 4× larger, and we have a clear product expansion path to serve them by Month 18.”

The difference: The practiced answer doesn’t dispute the investor’s math — it reframes the strategy as intentional focus, not limited vision.

Product Objections

“Your AI isn’t accurate enough” / “This doesn’t seem defensible technically”

Honest answer: “Our current accuracy is X% on benchmark Y. We know that’s not sufficient for full automation. The product is designed as a human-in-the-loop system where our accuracy provides an 80% reduction in manual work even at current performance levels.”

Practiced answer: Show the human-in-the-loop design. Demonstrate that you’ve shipped around the limitation. Point to customers who are using it today despite the limitation — because the partial solution still delivers 10× value.

The difference: Never claim accuracy you don’t have. Investors who later discover exaggeration do not just pass — they talk.

Competitive Objections

“What happens when [Large Company] builds this?” / “I just saw three companies doing exactly this”

Honest answer: “The large platform player is a real risk. Our belief is that they will build a generic version that satisfies 60% of use cases. Our moat is the integration depth and proprietary data that makes us work for the remaining 40% that requires specialization.”

Practiced answer: Name the competitor. Show you’ve done the analysis. Explain your specific differentiation — not “we’re better,” but “here is the one dimension where we are irreplaceable for this ICP.”

The difference: Founders who haven’t thought about competition are dangerous. Founders who have thought about it and have a clear-eyed answer are credible.

Team Objections

“You don’t have domain expertise” / “This seems like a technical team without business experience”

Honest answer: “We’re aware of the domain gap. We’ve addressed it by bringing on [Advisor/early-hire] who has [specific credential] and has agreed to [specific role]. We are also in conversations with [potential hire].”

Practiced answer: If the domain gap is real, acknowledge it, explain the mitigation, and ask: “What would you need to see from us to be comfortable with the team?”

The difference: Turning the question back to the investor converts a defense into a relationship. It also surfaces what would actually move them.

Economic Objections

“The unit economics don’t work at this price point” / “Your burn rate seems high”

Honest answer: Present the unit economics model transparently. Show which assumptions drive the most variance. Be specific about what happens to LTV/CAC when gross margin improves from X% to Y% at scale.

Practiced answer: “I agree the current CAC is high. It’s high because we’re in a direct-sales-only motion. The PLG tier we’re launching in Month 4 is designed to bring blended CAC down to $X. Here’s the model.”

The difference: Investors who object to economics want to see that you understand which levers to pull. Show the levers, not just the current state.

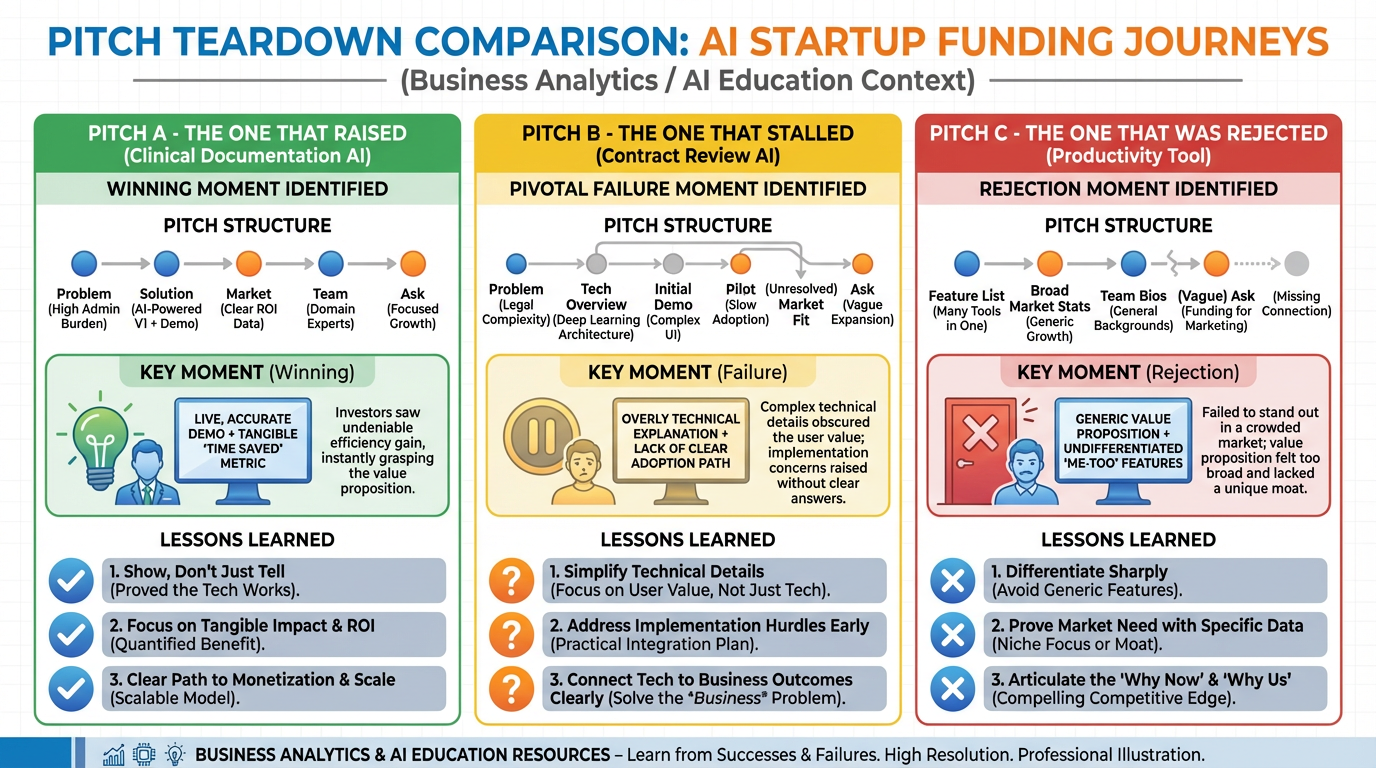

8Case Study: Three Pitches — One That Raised, One That Stalled, One That Was Rejected¶

Figure 9:Three pitch outcomes, three pivotal moments. The funded pitch won trust before slide 5. The stalled pitch had a great product and weak story. The rejected pitch had neither.

8.1Pitch A: The One That Raised¶

Company: An AI-powered clinical documentation tool for outpatient clinics.

What worked: The founder opened with a video — 42 seconds of a burned-out physician describing the two hours of daily documentation that was driving her to leave medicine. No investor in the room had experienced physician burnout personally. Every investor understood by the end of the video that the pain was real, serious, and costly. The founder then showed a live demo — a 90-second clip of the product converting a physician’s verbal summary into a complete SOAP note. The product worked, demonstrably, in the first five minutes.

The moment it won: Slide 3. The demo. Investors who needed convincing were convinced before the business case was presented. Everything after was confirmation, not persuasion.

8.2Pitch B: The One That Stalled¶

Company: An AI contract review platform for mid-market legal teams.

What stalled it: The product was genuinely excellent. The demo was polished. The unit economics were defensible. But the pitch opened with the architecture — a 10-minute walkthrough of how the NLP pipeline processed documents — before any investor had been given a reason to care about contract review. By the time the founder reached the pain and the market, the room had decided this was a feature, not a business.

The moment it stalled: Slide 1. The founder led with technology, not transformation. The investors passed. The company later re-pitched with a completely restructured deck leading with customer pain and raised the round within 60 days.

Lesson: A great product in a bad story structure looks like a bad product. Structure is not presentation hygiene — it is the argument itself.

8.3Pitch C: The One That Was Rejected¶

Company: An AI productivity tool for knowledge workers.

Why it was rejected: The TAM was cited as “the global productivity software market” — a figure derived from a single market research firm’s report. When an investor asked how many people would actually pay 2M.

The moment it was rejected: Q&A, first question. The inability to defend the market sizing without the research report was fatal. Investors are not buying a market research report. They are buying a founder’s conviction and evidence.

Lesson: Know the numbers from the inside out. If an investor removes your slides, you should still be able to make the entire case from memory.

9Lab 5: The Pitch¶

This is the culminating deliverable for the first half of the course. Every component builds on the work from previous chapters.

9.1Deliverable 1: Complete BMC Narrative (2 Pages)¶

Write a two-page narrative (not a filled canvas — prose) that explains all nine blocks of your Business Model Canvas with investment-grade specificity. For each block, the reader should understand:

What you chose and why

What you considered and rejected

What assumption drives the most risk in that block

Starter Prompt: “Given our target customer [ICP description] and our value proposition [description], help me think through the trade-offs between a PLG and sales-led channel motion, including the CAC implications for each.”

9.2Deliverable 2: 10-Slide Pitch Deck¶

Build a complete 10-slide pitch deck following the architecture from Section 5.4. Each slide must be designed and contain actual content — no placeholder text. The deck will be evaluated on:

Pain clarity (does the problem feel real and urgent?)

Transformation framing (does the solution feel inevitable?)

Investor-readability (is each slide legible at a glance?)

Structural integrity (does the sequence answer investor questions in order?)

Starter Prompt: “Review my slide 2 draft [paste content]. Score it on pain clarity from 1–10 and explain specifically what is missing from an investor’s perspective.”

9.3Deliverable 3: Working Demo (3–5 Minutes)¶

Build a functional prototype of your core product mechanic and prepare a 3–5 minute narrated demo. The demo must:

Show real input → real output (no static mockups)

Include at least one “magic moment” — the product doing something that would have taken a human significantly longer

Be narrated in narrator mode throughout

Starter Prompt: “I’m building a demo of [product description]. Help me identify the single most compelling ‘magic moment’ I should build toward, and suggest the minimum viable feature set to demonstrate it credibly.”

9.4Deliverable 4: Live Pitch to Panel (5-Minute Pitch + 10-Minute Q&A Defense)¶

Present your pitch live to a panel of evaluators. You will have 5 minutes to deliver the pitch and 10 minutes to defend it under questioning. Panels will use the five investor evaluation dimensions from Section 5.2. Evaluators may include faculty, external practitioners, or peer reviewers.

Evaluation criteria:

Transformation Framework (Steps 1–6 present and effective)

Demo execution (live, narrated, “magic moment” achieved)

Objection handling (answers are specific, honest, and practiced)

Ask clarity (amount, use, milestone articulated)

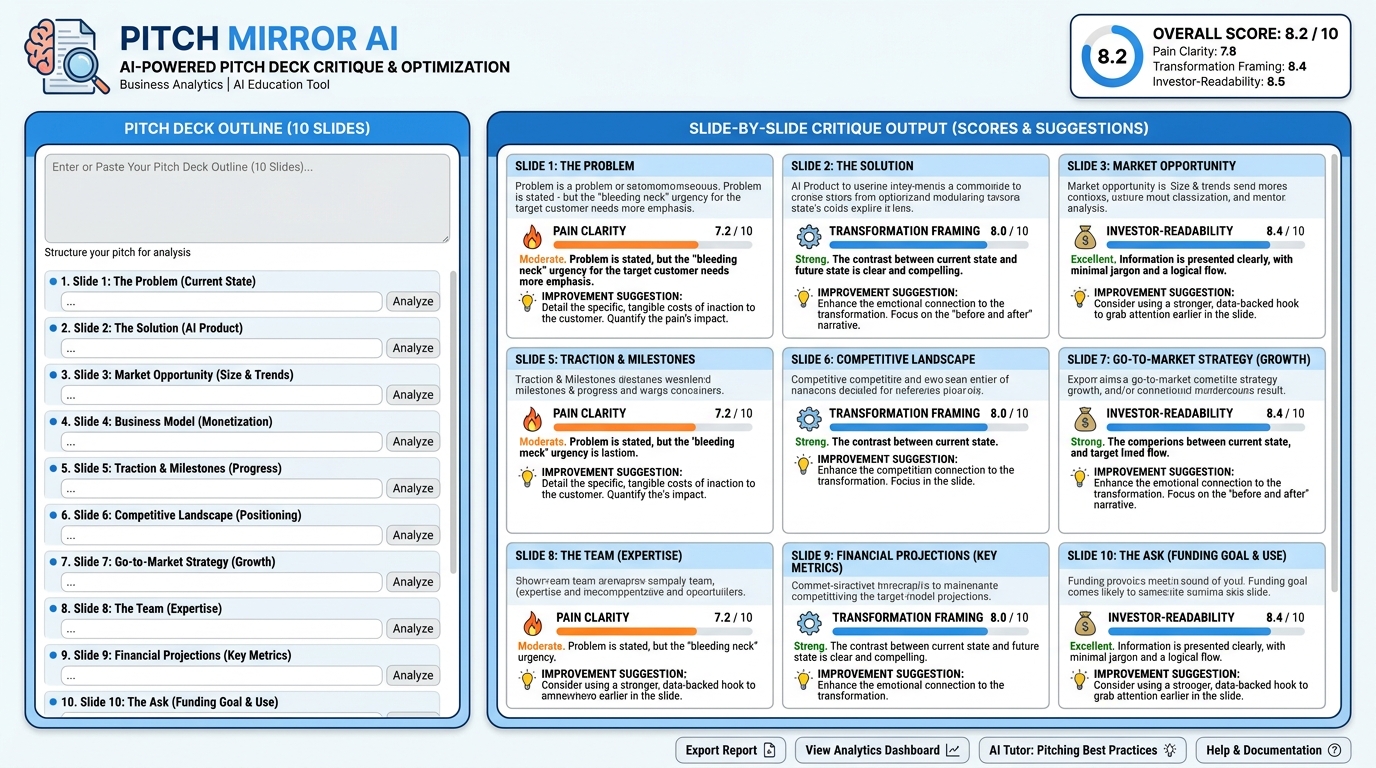

10AI Studio Build (Weekly): The Pitch Mirror¶

Figure 10:The Pitch Mirror app: a shareable web application that scores any 10-slide pitch deck against the architecture from this chapter, providing slide-level feedback across three dimensions. Built with AI Studio’s Build feature.

Capability Introduced: AI Studio Build — shipping functional web applications from natural language descriptions.

The Assignment:

Using AI Studio and its Build feature, design and ship a public web application called The Pitch Mirror. The app should:

Accept a 10-slide pitch deck outline as text input (one section per slide)

Analyze each slide against the 10-slide architecture from Section 5.4

Score each slide on three dimensions (1–10 scale):

Pain Clarity: Does this slide make the customer’s problem feel real and urgent?

Transformation Framing: Does this slide advance the “before/after” narrative?

Investor-Readability: Is this slide communicating its one job clearly?

Return a structured critique with specific improvement suggestions per slide

Generate an overall pitch score and the single most important fix

Run a Peer Review: After shipping your Pitch Mirror app, exchange deck outlines with a classmate. Run their outline through your Mirror and run your outline through theirs. Submit:

Your Pitch Mirror app URL (must be publicly accessible)

The peer review your Mirror generated for your classmate’s deck

A one-paragraph reflection on what your Mirror’s feedback revealed that you wouldn’t have noticed without it

Starter Prompt: “I want to build a web app called the Pitch Mirror. It takes a 10-slide pitch deck outline as input and returns slide-by-slide feedback. Help me write a thorough system prompt for this app that defines the evaluation criteria for pain clarity, transformation framing, and investor-readability — and generates structured output with numerical scores and specific improvement suggestions.”

11Discussion Prompts¶

11.1Prompt 1: The “Features First” Trap¶

Read the following claim: “Investors who don’t see the technical innovation first are not sophisticated enough to evaluate AI companies. The product should lead.”

Take a position and defend it using at least two scholarly sources published no more than two years old. Consider: at what stage of fundraising (pre-seed, seed, Series A) might the technical case carry more or less weight? What does the literature on investor cognition and decision-making suggest about narrative structure in high-uncertainty environments?

Post your initial response (minimum 350 words), then respond to at least two peers whose position differs from yours. Focus on the evidence — not the assertion.

11.2Prompt 2: Outcome-Based Pricing and Trust¶

Outcome-based pricing — charging customers a percentage of measurable value delivered — aligns incentives more closely than subscriptions or usage-based models. Yet very few AI companies use it.

Using at least two scholarly sources no more than two years old, analyze the conditions under which outcome-based pricing becomes viable for AI businesses. What trust mechanisms, measurement infrastructure, and contractual frameworks are required? Find one real example of a company that has implemented outcome-based pricing at scale and evaluate whether the model has held up under scrutiny.

Post your initial response (minimum 350 words), then respond to at least two peers, focusing on whether their examples hold up to the viability criteria you identified.

12Glossary¶

Business Model Canvas (BMC) A strategic management template created by Alexander Osterwalder that maps nine building blocks of a business model on a single page: Customer Segments, Value Propositions, Channels, Customer Relationships, Revenue Streams, Key Resources, Key Activities, Key Partnerships, and Cost Structure.

Channels The routes through which a company delivers its value proposition to customer segments, including direct sales, partner resellers, product-led growth, and digital platforms.

Customer Relationship Model The type of relationship a company establishes with each customer segment, ranging from fully automated self-serve to dedicated personal account management.

Product-Led Growth (PLG) A go-to-market strategy in which the product itself drives user acquisition, expansion, and retention — typically through freemium models, viral loops, or self-service onboarding.

Sales-Led Growth (SLG) A go-to-market strategy in which a dedicated sales team drives customer acquisition through outbound prospecting, enterprise negotiation, and centralized buying decisions.

Revenue Architecture The structural design of how a company generates income, including the combination of subscription, usage-based, and outcome-based models, tier design, and expansion mechanics.

Key Resources The most important assets required by a business model to deliver its value proposition, including physical, intellectual, human, and financial resources.

Key Activities The most important actions a company must perform to operate its business model and deliver its value proposition effectively.

Key Partnerships The network of suppliers, partners, and other external entities that help optimize the business model, reduce risk, or acquire resources.

Transformation Framework A six-step narrative structure for investor pitches: Paint the After Picture, Connect to Emotion, Explain the How, Anchor in Data, Prove You Can Win, and Make the Ask Specific.

The Ask The specific funding request in an investor pitch, including the amount, financial instrument (SAFE, note, equity), valuation or cap, use of funds, and the milestone the capital is designed to reach.

Narrator Mode A demo technique in which the presenter provides continuous verbal context about what is happening on screen and why it matters, converting a product demonstration into a story.

Investor Objection Taxonomy A classification of common investor objections into five categories — market, product, competitive, team, and economic — each requiring a distinct response strategy.

Outcome-Based Pricing A revenue model in which a company charges customers based on measurable outcomes delivered rather than seats, usage, or time.

SAFE (Simple Agreement for Future Equity) A financial instrument commonly used in early-stage startup fundraising that gives investors the right to receive equity at a future priced round, typically including a valuation cap and/or discount.

Defensibility The set of structural advantages — proprietary data, network effects, regulatory position, switching costs, or distribution — that protect a company’s market position from competition.

Demo Choreography The deliberate design of a live product demonstration, including the sequence of actions, the “magic moment” that creates peak investor engagement, and the contingency plan for technical failures.

Capital Efficiency A measure of how much value (revenue, milestones, market proof) a company generates per dollar of capital raised and deployed.

13Readings¶

Osterwalder, A., & Pigneur, Y. (2010). Business Model Generation. John Wiley & Sons. businessmodelgeneration

.com Ries, E. (2011). The Lean Startup. Crown Business. theleanstartup.com

Doerr, J. (2018). Measure What Matters. Portfolio/Penguin. whatmatters.com

Blank, S., & Dorf, B. (2012). The Startup Owner’s Manual. K&S Ranch. steveblank.com

Kawasaki, G. (2015). The Art of the Start 2.0. Portfolio/Penguin. guykawasaki.com

First Round Capital Review — review

.firstround .com — essays on pitching, fundraising, and company building from practitioners Y Combinator Startup Library — ycombinator

.com /library — canonical resources on pitch structure, investor relations, and early-stage strategy